Britain’s busy self-employed workforce, especially women, are missing out on millions of pounds in pension benefits. Support is here, but it’s also time for the government to help.

There are more than 4.3 million workers in the UK who are self-employed, equivalent to the combined populations of Manchester and Glasgow. This growing number of entrepreneurs provide everything from houses to haircuts, food deliveries to film-making, and contribute around £270bn a year to the UK economy.

Yet when it comes to one of the most important savings products on the market, a fund with enormous tax benefits that in the vast majority of cases well outpaces inflation over the long-term, around four in ten of our freelance workforce are missing out.

What is this miracle savings product? It is of course the humble pension…

Wait! Bear with us. We know the word ‘pension’ conjures up images of care homes, sedentary lifestyles and bingo, but the reality is very different.

Entrepreneurs are increasingly using pensions to fund active lifestyles from their mid-50s, whether global travel, paying down mortgages or as a mechanism to invest in new business ventures.

At Harmonic our experts work with many clients to put their pension to entrepreneurial use, including one who recently used their pension scheme to buy a commercial property - bringing enormous savings and efficiencies.

As life expectancy continues to rise, pension pots are stretching further and being put to ever more creative, and enjoyable use.

Even in the short-term, pension contributions count as an allowable expense. So just as items like business travel or office equipment can be deducted from taxable profits in annual tax returns and accounts, so can pension contributions.

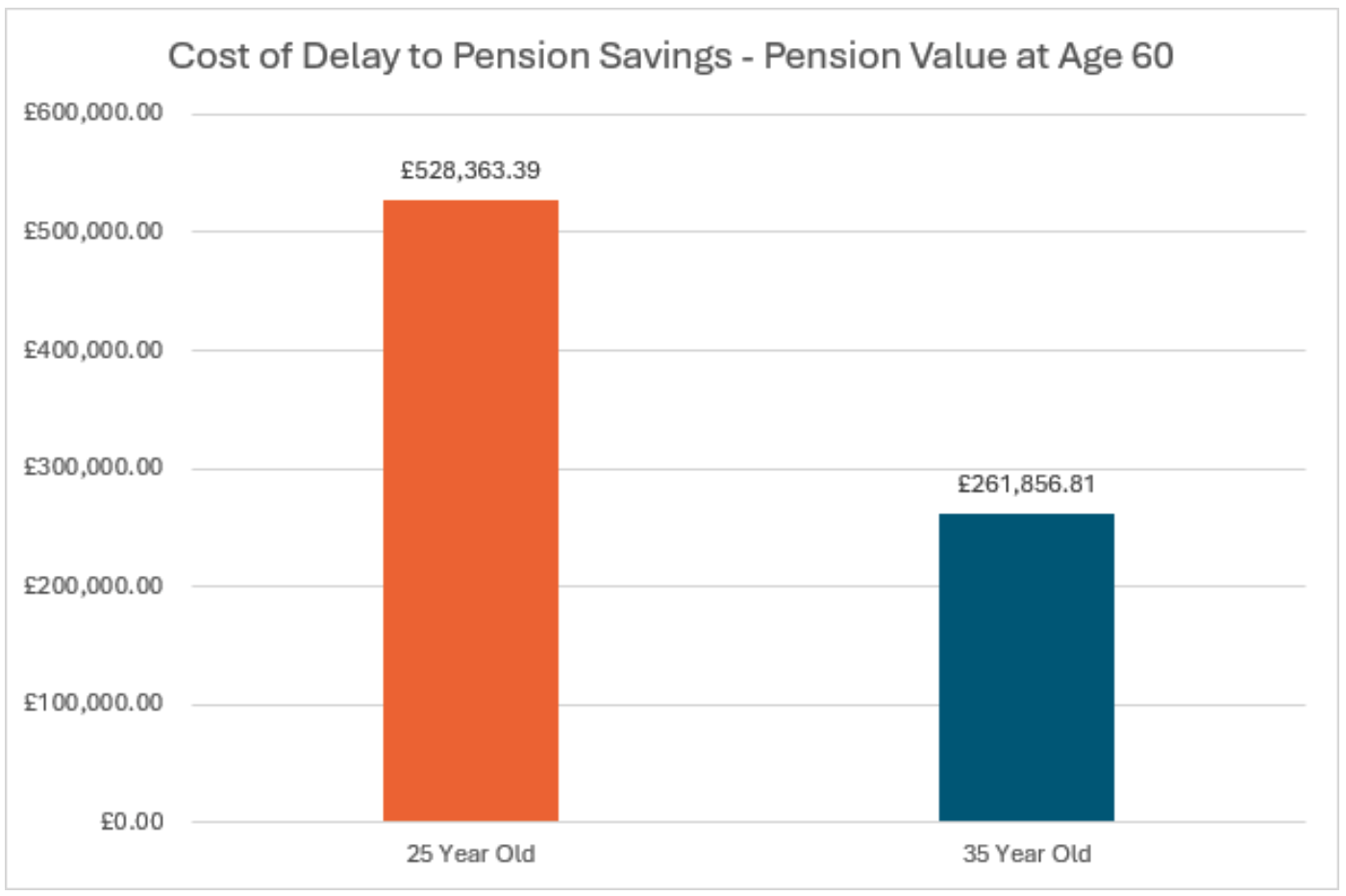

Table 1: Cost of delay to pension savings

For most entrepreneurs it is ultimately about the bottom line. And as Table 1 shows the longer we delay adequately saving for a pension the more we miss out – what is often termed as the compounding effect.

Table shows what happens if a 25-year old and a 35-year old both invested £10k in a pension and made the same contributions and experienced the same growth rate (6% p.a.). By age 60, the 25 year old would have over £250k than their decade-older colleague. That’s the remarkable impact of compound growth.

Pensions can also be used to invest across a range of sustainability themes such as climate change adaptation and mitigation, water infrastructure and the transition towards a cleaner less wasteful economy. So the self-employed workforce is also missing out on an important way to make a difference on these issues.

The price paid for the lost compounding effect affects some underrepresented groups more than others. When it comes to the self-employed market, it especially hurts women – who make up around a third of the UK’s self-employed workforce (with around 13% being self-employed mothers).

Official UK government estimates suggest women's private pension funds are 35% lower than men's, while one study found that by the time a woman reaches state pension age, they will have average pension savings of £69,000. This is £136,000 less than the average man, who will have saved £205,000.

We have a lot of self-employed clients at Harmonic and understand the many barriers that stop freelancers and small business owners from saving into a pension pot. These include (but are not limited to):

We plan to explore some of these barriers and ways to overcome them in future blogs, but the simple answer is to make sure you get the right support. All successful founders and freelancers know that success needs a team of people supporting you – whether associates, suppliers, employees or service providers, and the same is true of financial planning.

We think it’s time for the government to close this long-term savings gap for the self-employed.

The rollout of automatic enrolment since 2012 – which means employers are legally obliged to provide a pension for their employees – has led to a tenfold increase in total membership of relevant occupational pension schemes (from 2.1 million in 2011, to 21 million in 2019) – including bringing millions of women into pension saving for the very first time.

We urgently need an equivalent to automatic enrolment for the self-employed in the UK, or to consider other policy options such as changes to self-assessment tax returns or adjusting direct debit contribution defaults - as recently suggested by the Institute for Fiscal Studies.

This would be a vital first step in making sure our valuable freelance workforce have the same retirement prospects as employed workers.

If you are self-employed and would like to take your first step towards pension benefits, get in touch with our London team John Ditchfield and Sarah Dutton:

We'd welcome an initial discussion, and a first appointment can be booked using the links below.

If you require advice based on specific circumstances, contact our professional advisors.